Expedia Shares are Cheap, but it Might Be For Good Reason.

Expedia may be at risk of disruption due to AI.

This article is not investment advice, and is meant to be informative while entertaining. Before making an investment decision, consider your risk tolerance, and what may or may not be right for you.

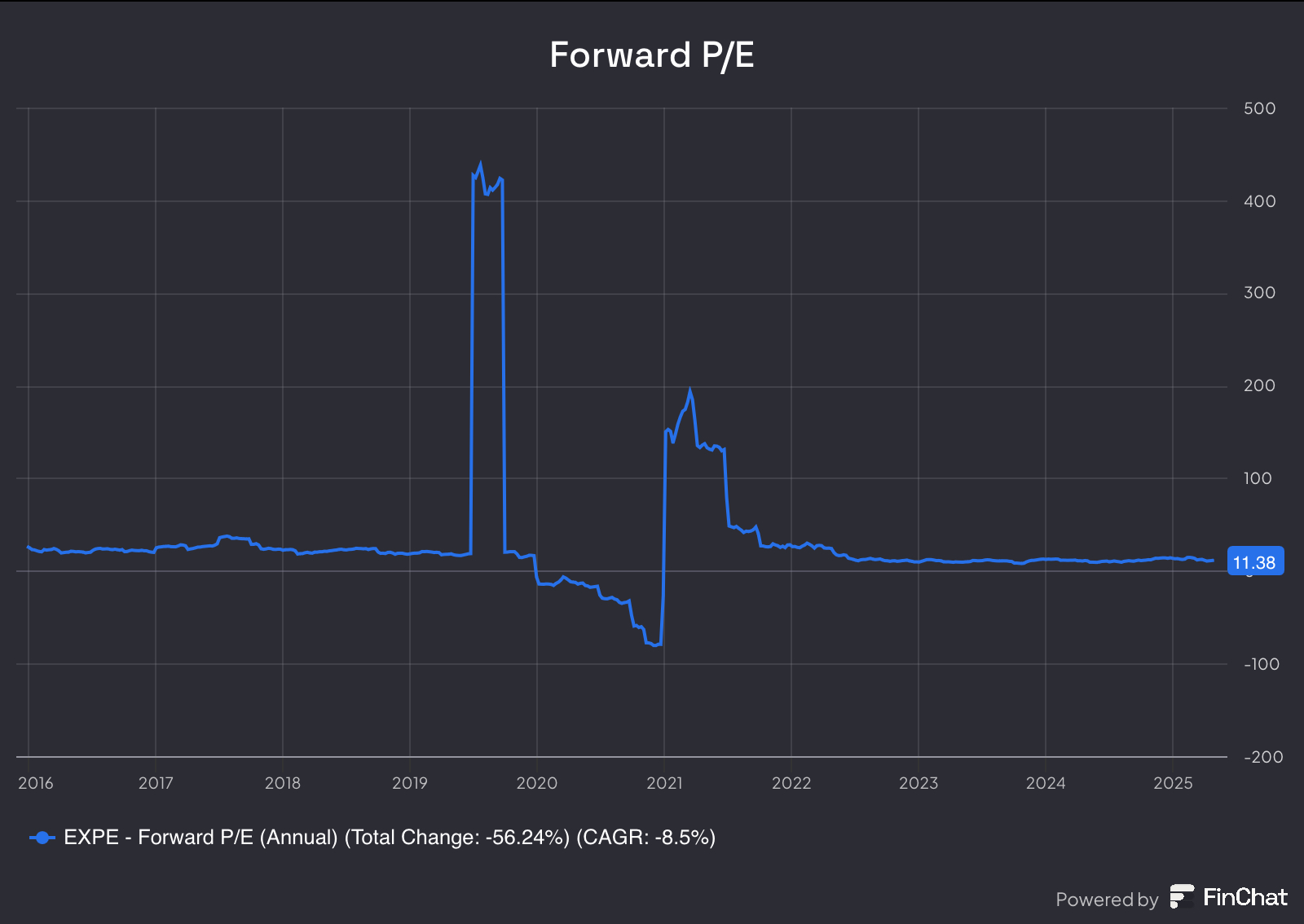

Expedia EXPE 0.00%↑ is a stock that has caught my eye recently, and I decided I needed to dig into it. On the surface, an 11x forward P/E for a stock that, pre-pandemic, traded at a mid-20’s forward P/E, seems like a steal. But, as always, I asked the question of “Why?” and after some digging I have my answer.

Today, I want to give a brief overview of Expedia’s business, a review of financial metrics, why they are trading at such a discount to a market multiple, and my final thoughts. Let’s start with the overview of Expedia’s business.

Business Overview

Expedia is an online travel company which owns brands such as Expedia, Hotels.com, and Vrbo. Their businesses allow consumers and businesses to book travel experiences, of which are offered by third parties, on their platforms. For example, through the Expedia app, I can book a hotel room, flight, and a rental car for a trip to Omaha, Nebraska, all in one stop.

They offer their products and packages of products, through three models: the merchant model, the agency model, and the advertising model.

Through the merchant model, they facilitate the bookings between the user and the lodging or other accommodation supplier. They do not bear inventory risk and have no control over the rooms. Most revenue under the merchant model is in the form of lodging.

Through the agency model, Expedia acts as the agent, passing the reservations made by the user to the travel provider. They then collect a fee for acting as an agent in the transaction. Most revenue under the agency model is related to air travel bookings.

The advertising model is self-explanatory, where they offer an advertising platform for advertisers. Much of this is done through a majority owned subsidiary, trivago.

In 2024, the merchant model accounted for 69% of revenue, agency model 23%, and advertising 8%.

In terms of travel accommodations, lodging accounts for the majority of their revenue, with advertising and air following behind.

The Financials

$20.64 billion market cap.

89.5% gross margins.

9% net margins.

0.8% dividend yield.

9% 10-year revenue CAGR.

11.6% 10-year EPS CAGR.

2.4x Debt-to-Equity

11% Return-on-Equity

Just a quick run down through the financials, the massive disparity between gross margins and net margins is because the majority of Expedia’s costs are classified as SG&A.

Expedia has just recently started paying a dividend, which I would expect to grow at a rapid pace over the next few years.

Top and bottom line growth has been strong, and has picked up post-pandemic due to the travel boom. If I had to venture a guess, growth will slow over the next few years, to no fault of Expedia’s but as travel demand continues to normalize.

Expedia is rather debt-light, has lots of cash on its balance sheet, and has a modest ROE. It’s a good business. At the most basic level, they act as a middleman. They don’t own or operate the hotels, airlines, car rental services, but facilitate the transactions between the people buying and selling. They’re the Uber of travel.

But, there’s a problem—they’re far from being like Uber. There’s a reason this stock is trading at 11x earnings, and it dawned on me after a couple of days of researching Expedia. I think Expedia is a great company, it has a lot of the characteristics I look for in a quality investment, but this is a classic case of where the numbers don’t tell the whole story.

A Quick Note on Valuation

While the chart is sort of wonky due to COVID, the above chart shows the forward P/E valuation of Expedia over the past 10 years. Pre-COVID, Expedia would often trade at a mid-to-high teens multiple, sometimes into the low 20’s. Post-COVID, it has been hovering around 9-12x. I often take this as a sign that the market is trying to tell us something, we just have to figure out if it is obvious or not. In this case, it dawned on me while on a walk.

Expedia is at Risk of Disruption From AI

Why is the Uber model brilliant? Because it connects drivers and riders seamlessly on the Uber app. No more calling a taxi service and waiting around for 20+ minutes for an old, smelly taxi to show up. In seconds on the Uber app you’ll be matched with a driver, know what they look like, what car they’re driving, and what past riders have thought of them.

Expedia does the same thing but with travel, right? Expedia connects users with hotels, airlines, and rental car companies to make travel arrangements. Like Uber, they simply offer the marketplace that you use. Well, it isn’t that easy.

You see, Uber drivers don’t have a website that you can call to specifically get them to show up to the bar to pick you up and take you home. It wouldn’t make sense—the same person doesn’t need to pick you up every time, and they probably don’t want to. For drivers to not be on the Uber app means they are completely missing out on business.

That isn’t quite the same story for Expedia. There’s nothing stopping me from booking a hotel room in the Hilton app so I get all the rewards points and discounts. Then heading over to Delta to get my flight. Expedia has introduced OneKey, which is their rewards program, and it does offer users discounts to use on travel.

But why would I book a trip on separate platforms when I could do it in one? Because in the future, you won’t be booking the trip, AI will. Agentic AI is the next step in the AI revolution. It will be your own personal assistant. There are already AI agents in use that can plan, schedule, and book trips. This category will grow like a weed.

Imagine if you could type into an AI prompt the following:

“Book me a trip to Boston, Massachusetts for the July 4th weekend. I am a Hilton Honors member, so find me a Hilton. I want a good deal, but I want to be close to downtown. Give me options to choose from before making a final decision. I also need a flight. I don’t care what airline, just give me the cheapest direct flight from Columbus. Also, recommend me some restaurants to check out, and fun things to do around the city. One last thing, I know I’ll need a reservation for that Friday night, so get me a reservation at a high-end steakhouse for 4.”

And boom. Your trip is planned. Your AI already has your credit card information, so it’ll take care of the checkout for you. If you think this sounds crazy, you’re in for a world of surprises a lot sooner than you realize.

And with that AI prompt, Expedia is useless. Why do I need anyone other than my AI agent to book my trips for me? If my AI can source the cheapest flights, best hotel rooms, and restaurants to check out in just seconds, oh and by the way it’ll be paid for without even thinking about it, then Expedia has serious problems.

Hopefully you can see why Expedia can be at risk of AI and Uber isn’t. These travel companies have their own websites with their own listings. In other words, they have scale, and while Expedia drives more sales to them, they don’t need Expedia to survive if AI is doing the booking. An Uber driver is someone and their car—no scale, so it is harder to AI-ify (did I just create the term AI-ify?).

My Final Thoughts

I am staying away from shares of EXPE. I really did want to buy this stock, but I think the 11x forward P/E is justified. I am sure it could revert upwards to a 15x and have good price performance, but I worry about long-term growth if they are competing with AI.

I don’t see any moat for EXPE, which makes it harder for me to buy as well. When you can book the same hotel on 10 other travel sites for likely the same price, what advantage do I have booking with Expedia? In fact, when I traveled to Atlanta for the college football national championship (Go Bucks), I booked my hotels through the Hilton app, and used Ubers around the city.

I think Expedia is a great company, but not one I want to own in my portfolio.